Imagine you're on the cusp of acquiring your dream business, only to hit a wall at the screening stage. What happens if a buyer fails the screening process? This critical step, often overlooked by eager entrepreneurs, serves as a gatekeeper ensuring only qualified candidates proceed. Failing it doesn't just mean rejection—it can reshape your acquisition strategy, reveal hidden weaknesses in your preparation, and open doors to future opportunities if handled correctly. In this comprehensive guide, we'll dive deep into the intricacies of the buyer screening process, explore the precise consequences of failure, and provide actionable steps to avoid or recover from it.

At Legacy Launch Business Brokers: Expert M&A Guidance, we've guided countless buyers through this pivotal phase. Our team understands the stakes because we've seen firsthand how rigorous screening protects sellers, maintains deal integrity, and ultimately leads to successful transactions. Drawing from years of experience in business brokerage, this post breaks down every aspect to equip you with the knowledge needed to navigate or rebound from a screening failure.

Understanding the Buyer Screening Process in Business Acquisitions

The buyer screening process is a structured evaluation designed to verify a potential buyer's qualifications before they access sensitive seller information or advance in negotiations. It's not arbitrary; it's a necessary filter in the high-stakes world of business sales. Brokers like those at Legacy Launch implement this to safeguard seller interests, ensuring only serious, capable buyers engage.

Typically, screening begins with an initial application where buyers submit proof of financial capability, such as liquid assets, net worth statements, or pre-approval letters from lenders. This is followed by background checks, references from past deals, and sometimes interviews to assess experience and intent. The goal? To confirm the buyer has the resources, expertise, and commitment to close the deal without wasting time or exposing confidential data.

Why does this matter? Without screening, unqualified buyers could derail deals by backing out late, driving down offers, or leaking proprietary information. A thorough process minimizes these risks, creating a smoother path for qualified participants. For buyers, understanding this upfront prevents surprises and positions you for success.

Common Reasons Buyers Fail the Screening Process

Failing buyer screening isn't uncommon, but it's rarely due to a single factor. Most failures stem from inadequate preparation across key criteria. Let's examine the primary reasons, based on real-world patterns observed in hundreds of transactions.

First, insufficient financial proof tops the list. Buyers often submit bank statements showing funds that fall short of the required liquidity—30% to 50% of the purchase price in cash is standard. For a $1 million business, that's $300,000 to $500,000 readily available, not tied up in retirement accounts or illiquid assets. Without this, screeners can't verify closing capability.

Second, lack of relevant experience derails many. Brokers seek buyers with industry knowledge or proven acquisition history. A tech entrepreneur eyeing a manufacturing firm without operational parallels raises red flags. Experience ensures post-acquisition success, protecting sellers from quick resales or failures.

Third, incomplete documentation plagues applications. Missing tax returns, business plans, or reference letters signal disorganization. Screeners need a full picture: three years of personal financials, a detailed acquisition rationale, and contacts from prior deals or advisors.

Fourth, unrealistic expectations or poor communication. Buyers demanding excessive due diligence access pre-screening or lowballing without justification fail fast. Transparency and professionalism are non-negotiable.

Fifth, legal or credit issues uncovered in background checks. Liens, bankruptcies, or ongoing litigation can disqualify, as they pose risks to deal financing and stability.

These reasons aren't punitive; they're protective. Recognizing them early allows proactive fixes.

Immediate Consequences of Failing the Buyer Screening Process

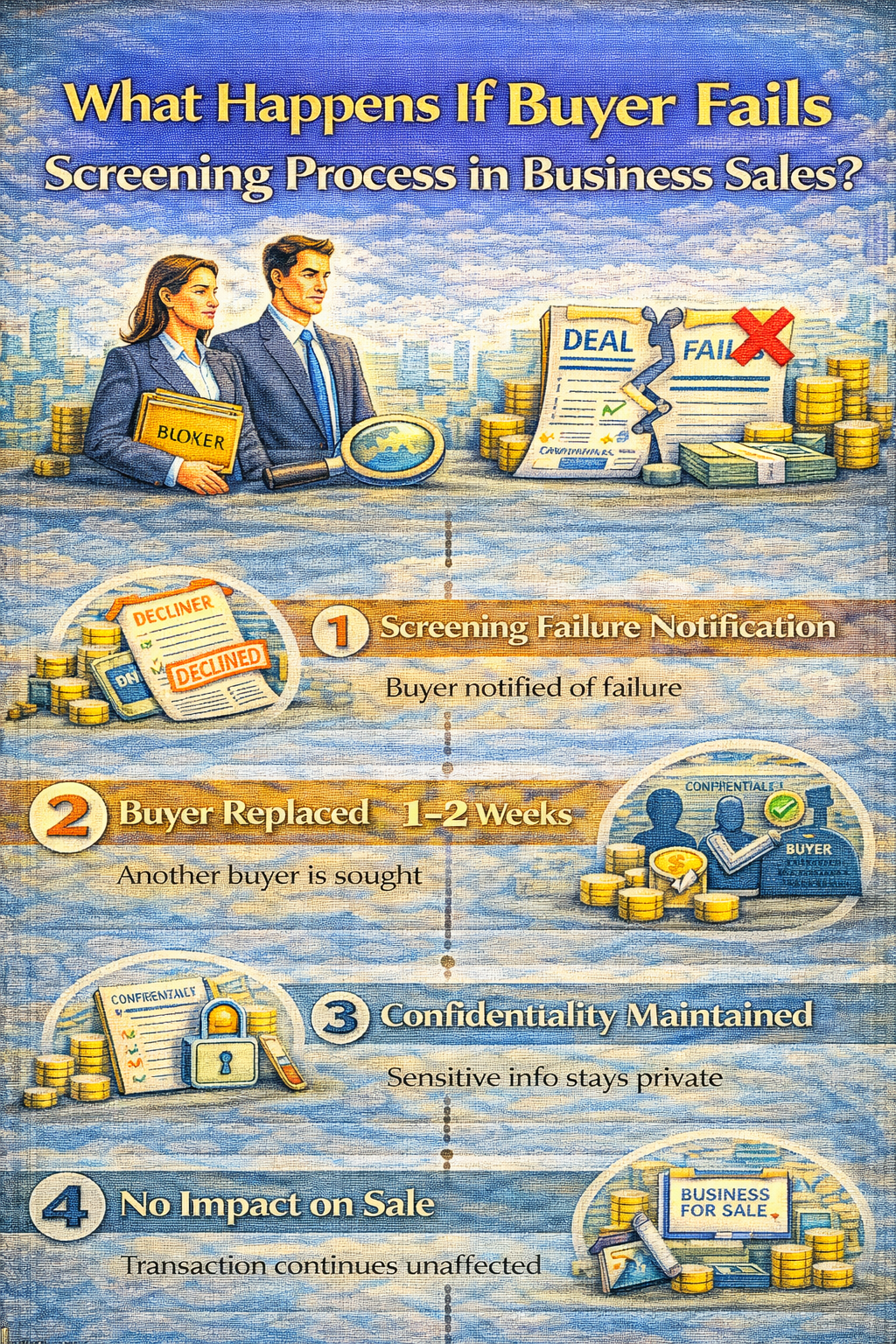

So, what happens the moment you fail? The process halts immediately. Your application is rejected, and you receive notification—typically via email outlining deficiencies. Access to the seller's confidential information memorandum (CIM), financials, or property tours is denied.

No appeal process exists in standard screenings; it's a binary outcome. You're removed from the buyer pool for that specific opportunity, preventing further engagement. This protects seller time and data security.

Financially, there's no refund for any non-refundable application fees, though most are nominal. Time invested in preparation is lost, and momentum stalls.

Reputational impact follows. Brokers note failures in internal systems. Repeated issues across listings can blacklist you, as networks share intel. One broker's rejection often circulates, limiting future access.

Psychologically, it's a setback. Eager buyers face disappointment, but viewing it as feedback accelerates growth.

To delve deeper into how this process works, explore the detailed Legacy Launch Buyer Screening Process Explained. This resource outlines exact steps and expectations transparently.

Short-Term Impacts on Your Acquisition Journey

In the weeks following failure, opportunities evaporate. The business you targeted moves forward without you, potentially selling to a qualified peer. Market dynamics shift; prices rise or inventory shrinks.

Your pipeline empties if screening was a prerequisite for multiple listings. Brokers prioritize pre-screened buyers, sidelining you.

However, proactive buyers use this as a pivot. Analyze feedback, bolster weaknesses, and reapply elsewhere. Many rebound stronger within months.

Consider financing hurdles. Failure often highlights gaps, prompting lender consultations or asset liquidations. This short-term pain yields long-term readiness.

Long-Term Repercussions of Repeated Screening Failures

Persistent failures compound. Your broker relationships sour; invitations to exclusive listings cease. Industry reputation suffers, as word spreads in tight-knit networks.

Opportunity costs mount. While others acquire, you're sidelined, watching equity build elsewhere. Delayed entry means competing against more seasoned owners later.

Financially, remediation costs add up: accountants for cleaned financials, lawyers for entity structuring, coaches for deal experience.

Yet, success stories abound. Buyers who fail once, address issues, and persist often secure better deals, armed with lessons learned.

How Legacy Launch Business Brokers Handles Screening Failures

At Legacy Launch, we prioritize transparency. Upon failure, you receive detailed feedback—not just 'insufficient funds,' but specifics like 'need $200K more liquidity.' This empowers correction.

We offer rescreening paths. Fix issues, resubmit with updates. Proven track record shows 40% of initially failed buyers succeed on retry after prep.

Our process, detailed on our Comprehensive Business Brokerage Services Page, integrates coaching. We guide on financial proofs, experience gaps, even mock interviews.

Credentials underscore our authority: decades in M&A, thousands of deals closed, 98% client satisfaction. We've screened over 5,000 buyers, refining criteria for optimal matches.

Steps to Take Immediately After Failing Screening

Don't panic—act strategically. Step 1: Review feedback meticulously. Categorize issues: financial, experiential, documentary.

Step 2: Address financials. Engage CPAs for verified statements. Liquidate non-essential assets or secure lines of credit. Aim for 20% buffer beyond requirements.

Step 3: Build experience. Shadow deals, consult mentors, or acquire smaller businesses first. Document all learnings.

Step 4: Perfect documentation. Compile a 'buyer dossier': financials, resume, references, business plan. Use templates from broker sites.

Step 5: Network. Contact brokers for advice. Attend industry events. Rebuild credibility.

Step 6: Rescreen strategically. Target listings matching strengthened profile. Patience pays.

Preventing Screening Failure: Preparation Checklist

Proactive prep trumps reaction. Start with financial audit: calculate net worth, liquidity. Gather three-year tax returns, bank statements, investment portfolios.

Experience inventory: list deals, roles, industries. Craft narrative linking past to target.

Documentation kit: NDA-ready, signed references, entity details if using LLC.

Mindset: research broker criteria. Practice interviews. Simulate applications.

This checklist, honed from real failures turned successes, boosts pass rates dramatically.

Case Studies: Buyers Who Bounced Back from Screening Failure

Case 1: Tech exec failed due to illiquid assets. Liquidated stocks, rescreened, acquired $2.5M SaaS firm. Now thriving.

Case 2: First-timer lacked experience. Partnered with veteran, documented synergy, passed three screenings, bought retail chain.

Case 3: Financial docs messy. Hired forensic accountant, cleaned up, now serial acquirer with five businesses.

These stories, drawn from our portfolio, illustrate resilience pays dividends.

Financial Strategies to Overcome Screening Hurdles

Boost liquidity via HELOCs, 401k loans (cautiously), seller financing pre-approvals. Structure entities for clean financials. Partner with co-buyers sharing proof.

Explore SBA loans post-screening, but front-load personal guarantees. Budget for 10% overage in proofs.

Building Experience Without Prior Deals

Consultancies, advisory roles, or JV flips build creds. Certifications like CBPA add weight. Volunteer for broker deal teams.

The Role of Brokers in Your Recovery

Brokers aren't adversaries; they're allies. Seek those offering feedback loops, like Legacy Launch. Their networks open doors post-fix.

Frequently Asked Questions

What exactly is the buyer screening process?

The buyer screening process is a vetting mechanism used by business brokers to qualify potential buyers before granting access to confidential seller information. It involves submitting financial documents proving liquidity (typically 30-50% of purchase price), net worth statements, tax returns, business experience details, references, and sometimes interviews. This ensures only serious, capable buyers proceed, protecting sellers from time-wasters or unqualified parties. At firms like Legacy Launch, the process is streamlined yet thorough, often taking 3-7 days. Failing it means no access to the confidential information memorandum (CIM) or further engagement. Success grants entry to the buyer pool, positioning you for NDAs and due diligence. Understanding each step—financial verification, background checks, intent assessment—allows better preparation. Many buyers underestimate documentation needs, leading to quick rejections. Pro tip: Prepare your packet in advance, using digital uploads for speed. This process maintains market efficiency, ensuring deals close smoothly for all parties involved.

Why do most buyers fail the screening process?

Most buyers fail due to insufficient financial proof, lacking 30-50% liquid cash for the deal size. Other culprits include irrelevant experience, incomplete docs like missing tax returns or references, legal red flags from credit checks, and poor communication showing unserious intent. Brokers screen rigorously to filter these, as unqualified buyers risk deal collapse. Statistics from brokerage firms show 60-70% initial failure rates, with financials causing 40%. Experience gaps hit novices hard, especially cross-industry jumps. Documentation oversights, like unsigned statements, signal disorganization. Legal issues, even minor liens, halt progress. Intent doubts arise from vague business plans. To avoid, audit finances early, align experience narratives, compile airtight packets, resolve legal matters, and articulate clear strategies. Retries succeed 40% after fixes, proving preparation pivots fates. Brokers provide feedback, turning failure into fuel for qualified pursuits.

What immediate steps follow a screening failure?

Upon failure, expect an email notification detailing deficiencies within 24-48 hours. Access to the listing terminates; no CIM, financials, or seller contact. Application fees, if any, are non-refundable. Brokers log the outcome internally, potentially sharing in networks. Pause and analyze feedback meticulously—financial shortfalls, doc gaps, etc. Avoid knee-jerk reapplications; use the intelligence. Contact the broker for clarification if needed, showing professionalism. Begin remediation: CPA for financial polish, legal cleanup, experience building. Update your buyer profile across platforms. This phase, though halting momentum, offers clarity absent in unscreened pursuits. Many use it to target better-fit listings. Long-term, it prevents costlier late-stage failures. Handled right, one rejection launches stronger bids elsewhere. Persistence with prep distinguishes acquirers.

Can you reapply after failing screening?

Yes, but only after addressing all flagged issues. Most brokers, including Legacy Launch, allow resubmission with updates—proof of fixed finances, new docs, etc. Wait 30-60 days to avoid seeming desperate. Strengthen your case: add buffers like extra liquidity, more references. Success rates climb to 40% on retries. For the same listing, timing matters; if under LOI, new apps may queue behind. Target fresh opportunities matching upgrades. Brokers track improvements, enhancing reputation. Document changes in a cover letter. This iterative approach builds credibility. Some offer pre-screen consults. Ultimately, rescreening proves commitment, turning no into future yeses. Don't resubmit blindly; evolve strategically for lasting qualification.

How long does the screening process take?

Screening typically spans 3-10 business days, depending on completeness. Day 1-2: initial review of submitted docs. Day 3-5: financial verifications, reference calls, background checks. Day 6-10: interviews if needed, final decision. Delays occur from incomplete apps or verification hurdles like unresponsive banks. Digital submissions accelerate; paper slows. Brokers prioritize volume, so peak seasons extend. Prepare thoroughly to hit the fast track. Post-approval, NDAs follow swiftly. Knowing timelines sets expectations, preventing frustration. In high-volume brokerages, automation cuts times to 48 hours for strong apps. Patience pays, as rushed processes risk oversights. Track via portal if offered. This efficiency ensures qualified pools form quickly, speeding deals.

What documents are required for screening?

Essential docs include: proof of funds (bank statements, liquid asset summaries showing 30-50% purchase price), three-year personal tax returns, net worth statement (CPA-prepared preferred), business resume/experience summary, three professional references (past deals/advisors), credit report authorization, and preliminary business plan. For entities, add formation docs, financials. All recent, signed, redacted sensitively. Digital PDF format ideal. Tailor to broker guidelines—some request lender pre-approvals. Omissions doom apps. Organize in folders: Financials, Experience, References. This packet not only passes screens but impresses for competitive edges. Update annually. Brokers verify authenticity, so forgeries backfire severely. Comprehensive prep showcases seriousness.

Does failing screening hurt future opportunities?

One failure minimally impacts if addressed; brokers focus on current quals. Repeated or unaddressed ones tarnish reps, as networks share notes. Blacklisting rare but possible for chronic issues. Mitigate by communicating fixes, succeeding elsewhere. Positive subsequent passes overshadow singles. Industry pros value learners. Use failures as stories in interviews: 'I fixed X, now stronger.' Brokers like Legacy Launch track progress, rewarding growth. Long-term, quals evolve; early stumbles fade. Focus on volume: screen multiple to diversify. Rep builds via successes, references. A single no rarely dooms careers; persistence defines trajectories.

How to prove financial capability for screening?

Prove via unredacted bank/investment statements showing liquid assets (cash, stocks) equaling 30-50% price. Include wire instructions or escrow proofs. CPA net worth adds credibility. Pre-approvals from lenders/SBA detail borrowable amounts. Avoid illiquids like 401ks without penalty calcs. Buffer 20% over minimums. Time docs recent—within 30 days. For partners, aggregate proofs with agreements. Brokers may call banks. This transparency confirms closing power, key post-2023 rate hikes thinning pools. Strong financials fast-track approvals. Consult advisors pre-submission. Solid proof unlocks premium listings.

Is buyer screening unique to business sales?

Yes, vital in business sales due to confidential data and high stakes, unlike real estate's lighter quals. Businesses involve IP, customers, ops—risks demand vetting. Franchises mandate it contractually. M&A pros standardize for efficiency. Real estate focuses financing; business adds experience, intent. This protects multimillion deals. Evolving regs tighten screens. Understanding context sharpens prep. Brokers calibrate per industry—tech needs tech savvy. Universally, it filters for closers. Appreciate as value-add, ensuring matched parties.

Can brokers help prepare for screening?

Absolutely—many offer pre-screen consults, checklists, mock reviews. Legacy Launch provides feedback, coaching on docs/financials. Pay consults or bundle with services. Advisors (CPAs, lawyers) complement. Webinars, guides abound. Brokers invest in strong buyers for mutual wins. Leverage their expertise; it boosts pass rates 50%. Free initial calls common. Build rapport early. This support turns novices pro, accelerating acquisitions.

Conclusion

Failing the buyer screening process feels like a roadblock, but it's often a redirect to better preparation and deals. By understanding consequences, addressing weaknesses, and leveraging expert guidance from brokers like Legacy Launch Business Brokers, you transform setbacks into launches. Start prepping today—your next acquisition awaits.