Are you a business owner wondering how to get started with exit planning? You've built something incredible, but transitioning out requires strategy to maximize value, minimize risks, and secure your future. This comprehensive guide draws from proven frameworks like the Value Acceleration Methodology, sharing actionable steps, real insights, and expert advice to launch your exit planning journey effectively.

At Legacy Launch Business Brokers: Expert Exit Strategy Partners, we specialize in guiding owners through this process. With years of hands-on experience facilitating smooth transitions, we've helped numerous entrepreneurs achieve their goals. This post builds on our detailed exit planning advice for business owners, offering expanded strategies and practical tools.

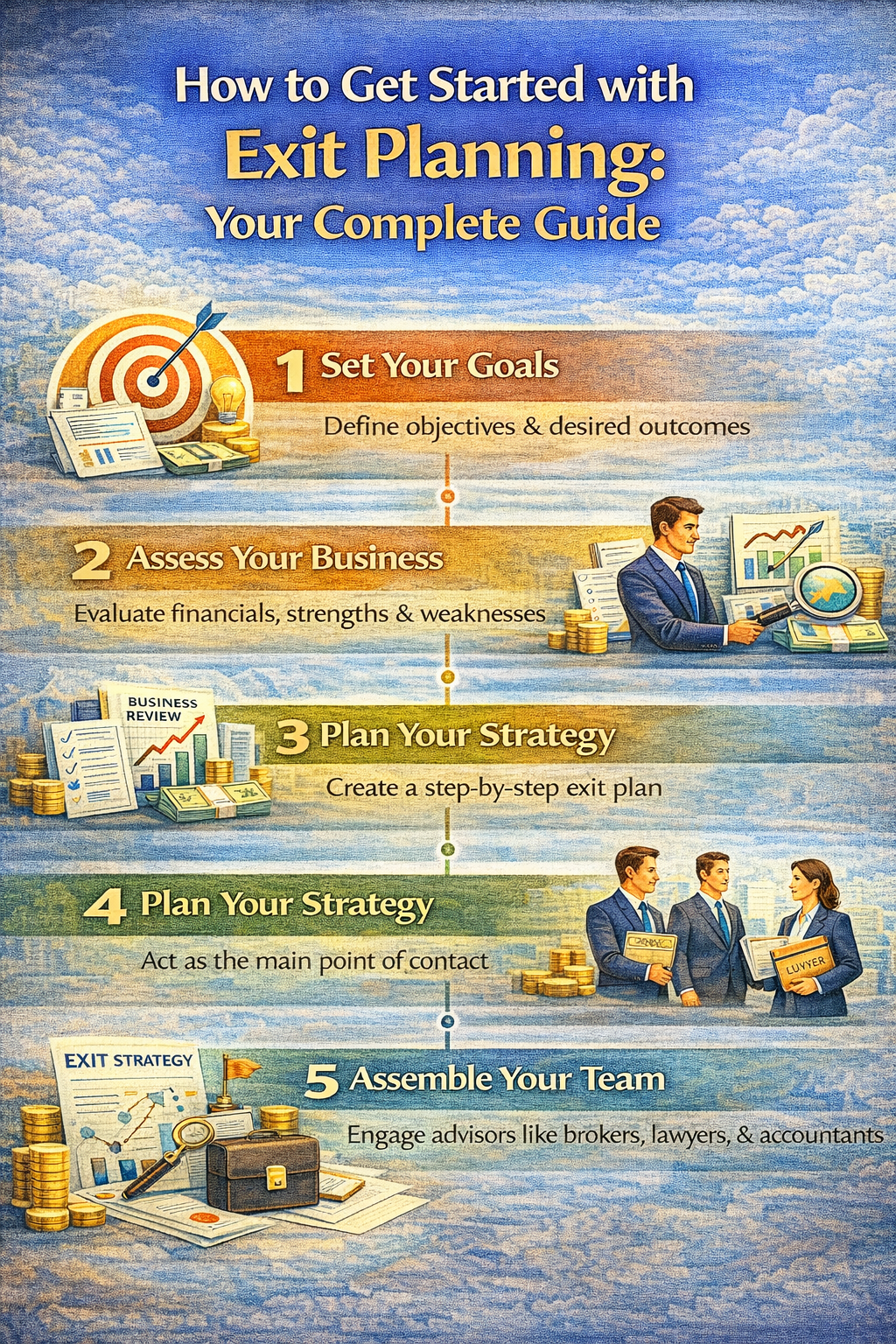

What Is Exit Planning and Why Start Now?

Exit planning is a strategic process where business owners prepare their company, themselves, and their stakeholders for the eventual transition of ownership. This could involve selling the business, passing it to family, or other strategies. It's about shifting from income generation to value creation, ensuring your business is attractive to buyers and aligned with your personal goals.

Why prioritize it early? Many owners wait until they're ready to exit, but statistics show that prepared businesses sell for 20-50% more. Unplanned exits often lead to rushed sales at lower values or family disputes. Starting now builds resilience against market shifts, health issues, or economic downturns. Think of it as a roadmap: the earlier you plot the course, the smoother the journey.

From our experience at Legacy Launch Business Brokers, owners who begin exit planning 3-5 years in advance report higher satisfaction and financial outcomes. We've seen businesses double in value through targeted improvements. Delaying can mean missing opportunities to enhance operations, finances, and market position.

Step 1: Define Your Personal and Financial Goals

The foundation of effective exit planning is clarity on your objectives. Ask: What does success look like post-exit? Do you want full retirement, semi-retirement, or a new venture? Quantify your financial needs—calculate the lump sum required for your lifestyle, accounting for inflation, taxes, and unexpected expenses.

Create a personal financial roadmap. List assets, debts, retirement accounts, and desired annual income. Tools like retirement calculators help project needs. For instance, if you need $200,000 yearly post-exit, factor in investment returns and Social Security. Align this with business value goals—aim for a sale price covering 10-20 times your annual expenses.

Consider non-financial goals too: legacy preservation, employee welfare, or philanthropy. Document everything in a one-page plan. Revisit quarterly as life changes. Owners often overlook emotional aspects; counseling can help process the identity shift from owner to ex-owner.

In practice, we've guided clients who discovered they needed $5 million more than expected, prompting value-building strategies years ahead. This step prevents misalignment, where the business sells but personal dreams falter.

Step 2: Assess Your Business's Current Value and Readiness

Next, value your business objectively. Use methods like discounted cash flow, comparable sales, or asset-based valuation. Engage a certified appraiser for accuracy—DIY tools give ballpark figures but miss nuances.

Key metrics: EBITDA multiples (often 3-6x for small businesses), revenue growth, customer concentration, and recurring revenue. A healthy business has diversified customers (no single client >15% revenue), strong management depth, and scalable systems.

Conduct a readiness audit: Review financials for clean books, operations for owner dependency, and legal for IP protection and contracts. Common pitfalls include key-person risk, where the business relies too heavily on you. Score your business on a 1-10 scale across value drivers like financial performance, operations, and market position.

Our team's audits reveal that 70% of businesses are worth less due to fixable issues like poor documentation. Early assessment identifies gaps, like building a management team or diversifying revenue, boosting value significantly.

Step 3: Build Your Professional Advisory Team

Exit planning demands experts: business broker, CPA, attorney, financial advisor, and possibly an M&A specialist. They form your quarterback team, coordinating efforts.

Choose based on experience with exits in your industry. A broker like those at Legacy Launch Business Brokers Professional Services brings market knowledge and buyer networks. CPAs handle tax strategies; attorneys structure deals to minimize liabilities.

Meet regularly—quarterly at minimum. Share your one-page plan. Budget 1-2% of business value for fees; it's an investment yielding multiples in returns. Vetting tip: Ask for case studies and references from past exits.

We've assembled teams that saved clients millions in taxes through structures like ESOPs or installment sales. A cohesive team prevents silos, ensuring holistic planning.

Step 4: Enhance Business Value and Transferability

Focus on eight value drivers: financials, operations, marketing, human capital, customer base, systems, competitive advantage, and owner transition. Implement improvements systematically.

Financials: Normalize earnings by adding back personal expenses. Operations: Document processes to reduce owner dependency—aim for 90-day vacations without issues. Marketing: Build brand and pipeline.

Set KPIs: Increase EBITDA 20% yearly, reduce customer concentration. Invest in tech for efficiency. Recast financials to show true earning power.

Case in point: A client boosted value from $2M to $4.5M by professionalizing operations and diversifying clients over two years. These steps make your business 'buyer-ready,' appealing to strategic or financial buyers.

Step 5: Develop and Execute Your Exit Strategy

Choose your path: sale (strategic, financial, or individual buyer), family succession, management buyout, or liquidation. Each has pros/cons—sales maximize cash but require prep; succession preserves legacy but demands training.

Craft contingencies for illness or death: buy-sell agreements funded by life insurance. Timeframe: 1-7 years typical. Market your business confidentially via teaser memos.

Due diligence prep: Organize data rooms with financials, contracts, and projections. Negotiate terms favoring you—earn-outs tie to performance.

Post-exit: Plan reinvestment, taxes, and life transition. We've closed deals where owners netted 30% more through smart timing and buyer matching.

Common Mistakes to Avoid in Exit Planning

Avoid emotional decisions, ignoring taxes (up to 40% bite), or poor timing. Don't neglect team communication or legal pitfalls like unresolved lawsuits. Overvaluing based on gut feel loses deals. Procrastination is worst—70% of owners have no plan.

Track progress with annual reviews. Stay flexible—markets change.

Measuring Success in Your Exit Planning Journey

Success metrics: Achieved sale price, smooth transition, financial security, personal fulfillment. Post-exit surveys show planned exits yield 2.7x higher proceeds.

Regular benchmarking against peers keeps you on track.

Frequently Asked Questions

How long does exit planning typically take?

Exit planning usually spans 3-7 years, depending on business size, readiness, and goals. Early starters allow time for value growth, like improving EBITDA or reducing owner dependency. For a $5M business, 5 years might involve year 1 assessment, years 2-4 enhancements, and year 5 execution. Rushed plans risk lower values—prepared owners fetch 20-50% premiums. Factors include market conditions and exit type; family successions take longer for training. Track milestones quarterly. Advisors accelerate via proven frameworks, ensuring you're buyer-ready without stress. Our clients average 4 years, netting optimal results through phased execution. Patience builds wealth—start today for tomorrow's legacy.

What are the costs involved in getting started with exit planning?

Initial costs range from $5,000-$20,000 for valuations and team assembly, scaling to 1-5% of sale price for full services. Valuations cost $3K-$10K; advisors bill hourly ($300-$600) or retainers. Brokers take 5-10% commissions post-sale. Budget for legal/tax ($10K+). Total ROI: Enhanced value covers fees exponentially. Free self-assessments start you off. Factor ongoing costs like system upgrades. High-quality teams save via tax strategies (20-40% savings). Compare: Unplanned exits cost 30% in lost value. Invest strategically—our services deliver measurable uplift, with clients recouping investments quickly through higher multiples. Transparency ensures no surprises; detailed proposals outline fees upfront.

Do I need a business valuation to begin exit planning?

Yes, a professional valuation is essential as step one, providing baseline worth and growth roadmap. It uses methods like DCF or multiples, revealing gaps in financials or operations. Without it, strategies lack data—owners often overestimate by 50%. Costs $3K-$15K; update annually. It benchmarks progress, attracts advisors, and justifies pricing. For sales, buyers demand it anyway. Self-tools suffice initially but pros uncover hidden value. In our experience, valuations identify quick wins like normalizing add-backs, boosting figures 15-30%. Pair with readiness audits for full picture. It's your compass—navigate confidently.

How can I make my business more attractive to buyers?

Focus on transferability: Minimize owner dependency via documented systems and strong teams. Clean financials with normalized earnings show true profitability. Diversify revenue/customers, scale operations, protect IP. Boost recurring revenue for stability. Achieve 20%+ EBITDA growth. Marketing: Strong brand, pipeline. Legal: Clean contracts, no disputes. Buyers seek 'absentee owner' potential. Implement KPIs, tech upgrades. Case: Client added $1M value via CRM and management hires. Audit annually; advisors guide. Result: Higher multiples (4-8x vs. 2-3x). Preparation sells faster, at premiums.

What role does a business broker play in exit planning?

Brokers quarterback the process: Valuing, marketing confidentially, finding buyers, negotiating. They access networks, handle due diligence, maximize price/terms. Fees: 5-12% commission. Expertise prevents pitfalls like lowball offers. Unlike agents, brokers manage full lifecycle. They advise pre-sale improvements for 20-50% value lifts. Our Legacy Launch brokers match buyers perfectly, closing deals 30% above initial vals. Essential for complex sales; DIY risks revenue loss. Partner early for strategy.

Can I do exit planning without professional help?

Possible for simple cases, but pros yield 2-3x better outcomes via expertise in tax, legal, valuation. DIY misses nuances like earn-out structures or liability shields. Use templates for goals/audits, but scale limits depth. Stats: Advisor-led exits net 71% higher proceeds. Time saved alone justifies cost. Start solo, engage when selling. We've seen DIYers undervalue by 40%; teams optimize. Hybrid: Self-assess, pro-execute. Resources abound, but experience trumps. For max success, build your team.

What tax strategies are key in exit planning?

Minimize via structures: Installment sales defer gains; ESOPs offer deductions; gifting reduces estate tax. QSBS excludes $10M gains. Charitable trusts. Timing sales to low brackets. Recapture depreciation. State taxes vary. CPAs model scenarios, saving 20-40%. Pre-exit: Build basis, normalize. Post: Roth conversions. Our clients saved $500K+ via entity choices (LLC to C-corp). Plan 2+ years ahead; IRS rules strict. Integrate with financials for holistic impact. Essential for net proceeds.

How do I prepare for life after exiting my business?

Define purpose: Travel, hobbies, boards, startups. Financially: Diversify proceeds into portfolios yielding 4-7%. Estate plan for legacy. Emotional: Therapy for transition. Trial runs: Month-long absences. Build networks. Budget 'fun' funds. Clients thrive with plans including philanthropy/volunteering. Advisors craft post-exit strategies aligning wealth/life. Avoid 'sudden wealth' pitfalls via spending plans. Measure fulfillment yearly. Transition is chapter two—plan vibrantly.

What if market conditions are poor for selling now?

Focus inward: Build value regardless—strong businesses weather storms, sell anytime. Use time for audits, team building, financial cleanup. Contingencies ready. Monitor multiples (track peers). Diversify buyers. Historical recoveries reward patience—post-2008, prepared sold 50% higher. Advisors time optimally. Don't force; enhance transferability. Our guidance turned downturns into 2x value gains. Markets cycle—position ahead.

How often should I review my exit plan?

Annually or on triggers: Life events, market shifts, valuation jumps. Quarterly check-ins with team. Update goals, metrics. Business evolves—30% plans outdated yearly. Milestones: Value growth, dependency reduction. Software tracks progress. Flexibility key. Clients reviewing regularly adapt, achieving 90% goals. Proactive beats reactive. Schedule now.

Ready to Launch Your Exit Planning?

Getting started with exit planning empowers you to control your destiny. Begin with goals, value your business, assemble experts, and execute relentlessly. Visit Legacy Launch's exit planning advice hub for more. Your legacy awaits—act today.